TMRC Investment Thesis

Investments I look for take two forms. Best in class operators with a deep moat, or asymmetric opportunities. I'm defining an asymmetric as something with an upside that outweighs potential downside by a significant multiple.

In general, risk in finance is misunderstood. Standard deviation and beta are common measures of risk that I don’t believe accurately represent the risk of an investment. Standard deviations weight upside and downside volatility the same. Similarly, beta tracks the volatility of a stock compared to a benchmark and does not differentiate between the direction of said volatility. These measures are useful for evaluating how much an asset moves, but truly defining risk requires a more nuanced approach to assign values to any potential upside or downside, a process that is open to the interpretation of each analyst and will never be easily represented by one formula for all situations. Gauging risk by looking only at measures of average volatility is a foolhardy approach.

Investors should be looking for opportunities where the upside volatility exceeds the potential downside volatility which provides a better risk-return profile despite ranking high on traditional measures of risk.

This brings me to Texas Mineral Resources (TMRC), a micro cap miner focused on rare earth minerals (REM). TMRC has no real revenue or expenses. The thesis here will focus on the assets owned and their potential for monetization. This report will lay out how that would happen, why I think it's highly likely, and what the market opportunity is. Nothing I say here is investing advice. I own a position in the security mentioned.

Investment: Texas Mineral Resources (TMRC)

Market Cap: $145mm

Trade: Buy

Date: 2/11/22

Beta: 0.87

Company Overview

TMRC trades over the counter with a market cap of ~$150mm and average daily volume of 172.7k.

TMRC is owned 20% by insiders with another 20% owned by the Navajo Energy Transition Fund. Information on the rest of their ownership structure is not readily available but it seems that institutional ownership is negligible, leaving ~60% to retail and private funds.

Net insider selling is a bit concerning, but the volume is low and the insiders still own large amounts of the stock. Nobody has sold out of their position in a meaningful way. This should be taken into consideration since this report will discuss the likelihood of an event driven valuation.

Texas Mineral Resources' key asset is their 20% ownership of the Round Top mine in west Texas. Privately held USA Rare Earth (USARE) owns the other 80%. TMRC also has 100% interest in a mineral reclamation subsidiary, a 50.5% silver exploration JV, and has received 5 government grants on a variety of rare earth mineral (REM) related initiatives. To be conservative with this analysis this report will assume $0 value for non-Round Top ventures.

Round Top Mine

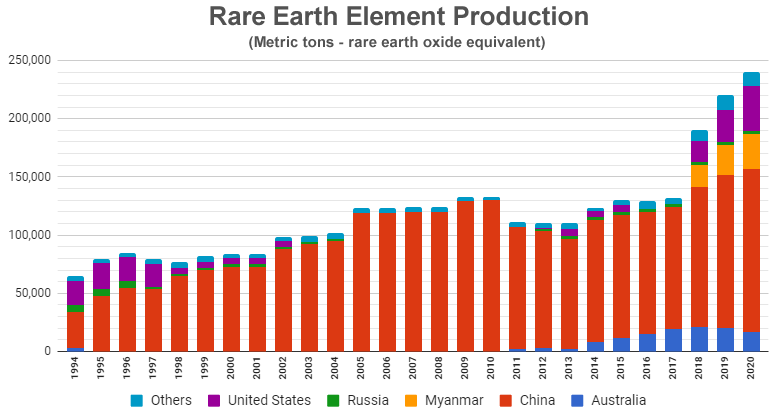

There are two REM mines in the United States. The Round Top Mine in Texas and Mountain Pass Mine in California. There are no domestic REM processing facilities (where raw materials are developed into usable components). Mountain Pass Mine is owned by MP Materials Corp (MP), which went public via SPAC in 2020. Mountain Pass Mine is currently operational, unlike Round Top.

In 2020, Mountain Pass Mine produced 38,500mt of REM (15% global production). A Chinese company has a 7.7% stake in MP and MP sells 100% of their REM to China. MP is planning on onshoring the processing in 2022, but there is nothing currently operational.

REM’s are critical components of a variety of advanced technologies. EV, consumer electronics, semiconductor, renewable power, and defense industries rely on them and there are no replacements. China is both the largest producer and consumer of REM’s, giving them leverage over the US economy.

This leverage has been noticed by the US government, and bipartisan legislation is now in effect to ban defense contractors from purchasing REM from China by 2026. China has weaponized their REM monopoly in the past, banning REM exports to Japan for 40 days over a territorial dispute. This is an additional risk given the contentious situation in Taiwan.

Contrasting this mandate with the actual state of US REM extraction and processing, significant domestic investment is needed in the near term to meet this goal. The bill also mandates the US begin stockpiling REM due to its strategic importance.

Impending legislation isn’t an investing thesis, but this aligns with the strategic importance of REM and the roadmap to get there. Over the past several years the US has acknowledged the need for strategic autonomy with key components in supply chains. Government funding and tax incentives are being utilized to drive domestic semiconductor production, and REM’s fall under the same category as critical inputs to advanced technology.

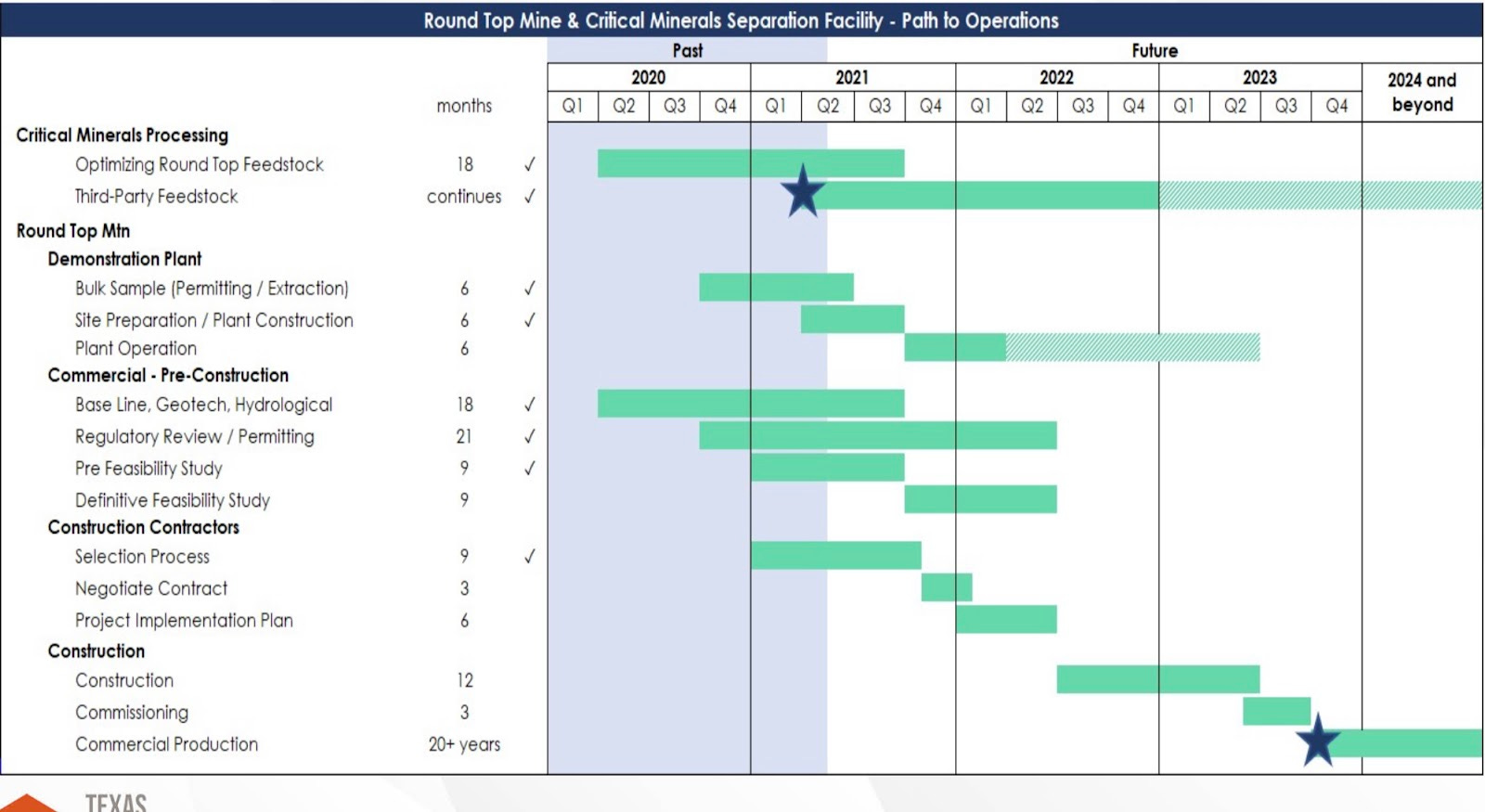

Environmental concerns have delayed production at Round Top. REM mining is a dirty process, and environmentalists argue that the mine could cause damage to the local ecosystem. These environmental concerns have delayed the mine in the past, but 2020 and 2021 have seen development. USARE has conducted several environmental studies relating to water pollution, animal protection, and waste management (USARE is financing these studies, a condition of the deal with TMRC to acquire the 80% stake). Progress is being made, and USARE expects to begin production on the mine by 2023.

Corporate timelines aren’t definitive, the takeaway is that development has been delayed due to environmental concerns. Geopolitical focus on securing critical components of tech supply chains has enabled progress, and may outweigh the potential environmental concerns enough to allow mining to commence.

According to USARE:

“The Round Top Deposit hosts 16 of the 17 rare earth elements, plus other high-value tech minerals (including lithium), including 13 of the 35 minerals deemed “critical” by the Department of the Interior and contains critical elements required by the United States, both for national defense and industry. Round Top is well located to serve the US internal demand. In excess of 60% of materials at Round Top are expected to be used directly in green or renewable energy technologies.”

Given the importance of these minerals, and the cooperation of USARE and TMRC, it is unlikely that this proven deposit of REM will not be utilized.

Financial Analysis

TMRC’s financial statements do not provide much insight, as the company is not currently revenue producing and the only expenses are related to exploration and G&A. As of 11/30/21 (most recent 10q), TMRC has ~$5mm in cash, no debt, and has burned through $37mm of the $42mm they’ve raised in equity. They have no revenue, and ~$410k in opex for the quarter (17% exploration costs, 83% G&A). They have quarterly grant income of $70k from a DOE contract to explore producing REM from coal waste.

TMRC’s 20% interest in Round Top is consolidated into a separate entity called RTMD. USARE controls the remaining 80%. This entity controls the mineral lease, the water lease, the surface purchase option, the surface lease, the bill of sale, and contracts/permits. Basically, the RTMD entity has total legal/economic ownership of the Round Top mine.

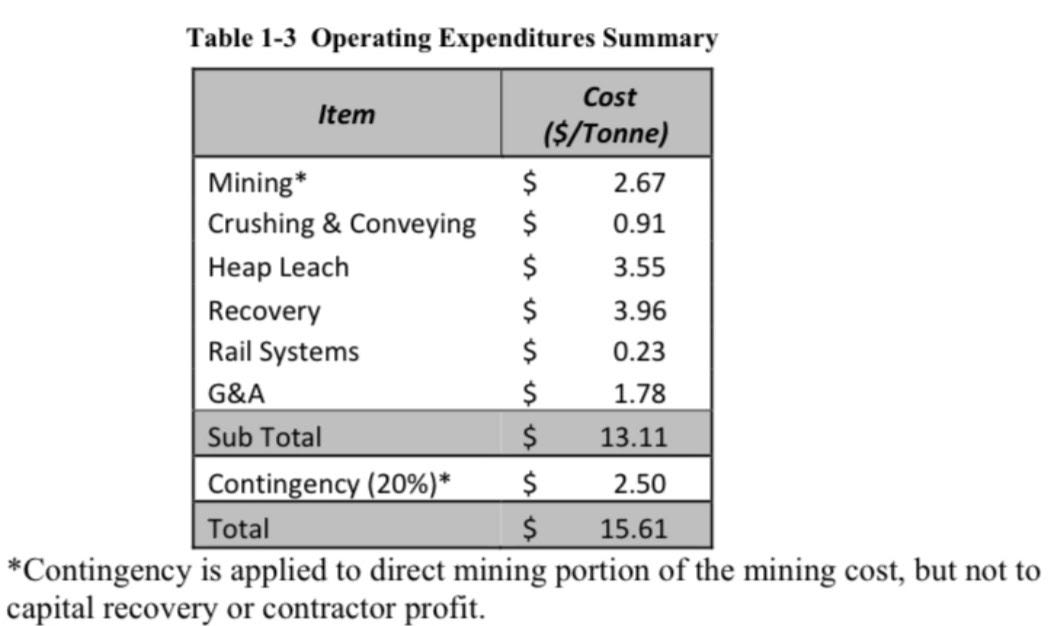

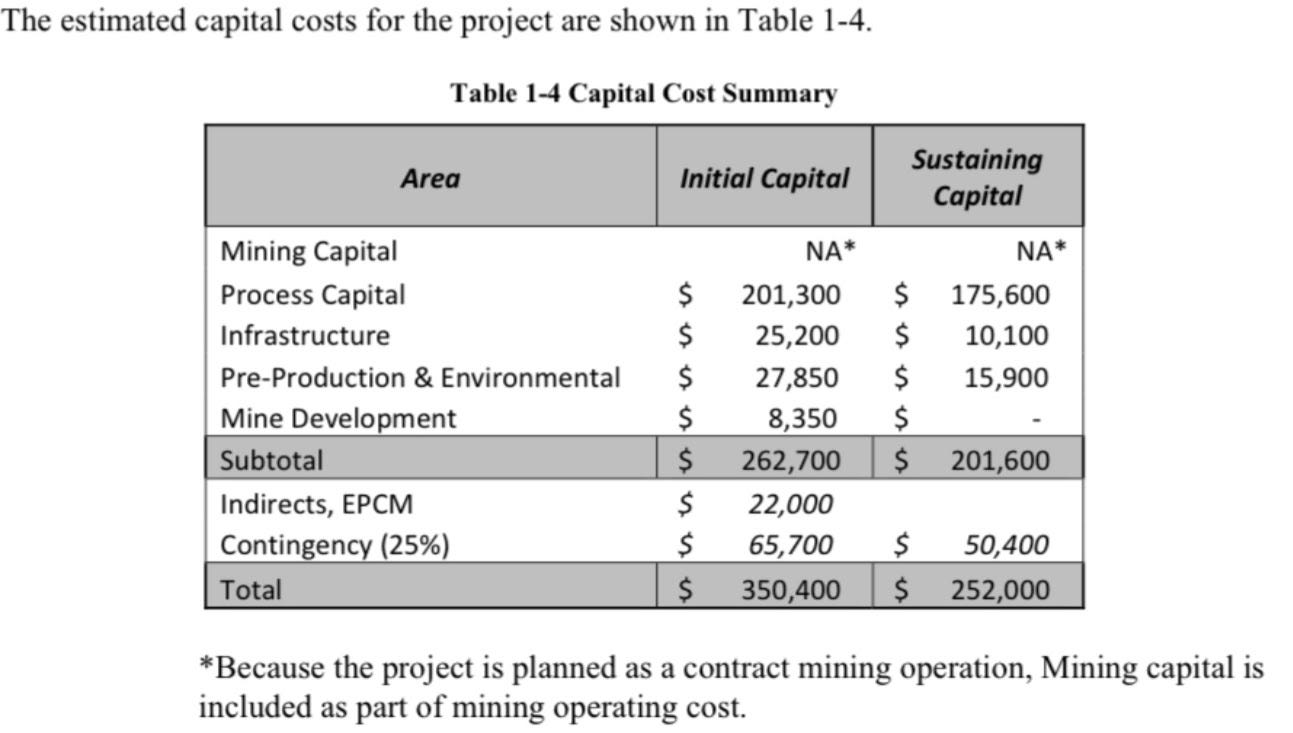

This 20-80 split of the mine reflects the capex and the profit split. There will be an estimated capex of $250mm over the life of the mine, which TMRC will bear 20% of. Same applies to revenues from sale of materials. Below are estimated opex and capex for the mine:

RTMD effectively has a 19 year lease on the land (its two different 19 year leases for the mine and some adjacent land). The lease lasts for 19 years once the mine begins producing “paying quantities.” The mine owes 8% of all uranium and fissionable materials, and 6.25% royalty on all other materials (royalty payable to the State of Texas). Fissionable minerals (uranium, plutonium, thorium) aren’t rare earth elements, but are often found in REM deposits.

Valuation

There are a couple different ways to look at valuation here. I see a financial opportunity, but valuing a mineral resource is a unique challenge because the value is in mineral resources that are not currently being extracted. I'll try a couple different approaches and paint a picture of the opportunity.

Approach #1:

Take the company’s word for the value of the mine. This (above) is from TMRC’s investor deck and has circulated around the internet - (NPV of $1.56bn x 20% share of the project)/ 71mm shares outstanding gives a NPV per share of $4.39. This represents a ~2x return on current prices if you assume a NAV multiple of 1.

Management used a strong implied operating margin of 71%. This is in contrast with a -26% margin for MP Materials Corp in 2020. This figure is misleading because MP had a $66mm non-operating settlement charge. Adjusting this out, the margin moves 5,000 bps to ~24%.

MP had quarterly operating margins of 36%, 44%, and 54% (Q1-3 2021). Still a ways away from 71%, but seems to be moving in the right direction. The Mountain Pass mine is much older (opened in 1952), so the extraction techniques are likely outdated. This results in lower efficiencies- lower yields and higher extraction costs. I'm not a mining expert and don’t know if this large difference can be accounted for with new technology. It’s something to note.

Approach #2:

In my opinion, the best approach would be to compare the resources between the Mountain Pass and Round Top mines and make a market cap comparison. However, there is not much information regarding the size of the deposit. In a research study (paid for by USARE) there are no definitive resource estimates.

The study frequently repeats the line that “Inferred mineral resources are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves.” This may be standard language when a resource has not yet been tapped and there is nothing more than exploratory activity, but this can’t be said definitively. The Mountain Pass mine doesn’t have any publicly available resource information available. Given the incomplete information, some assumptions are necessary.

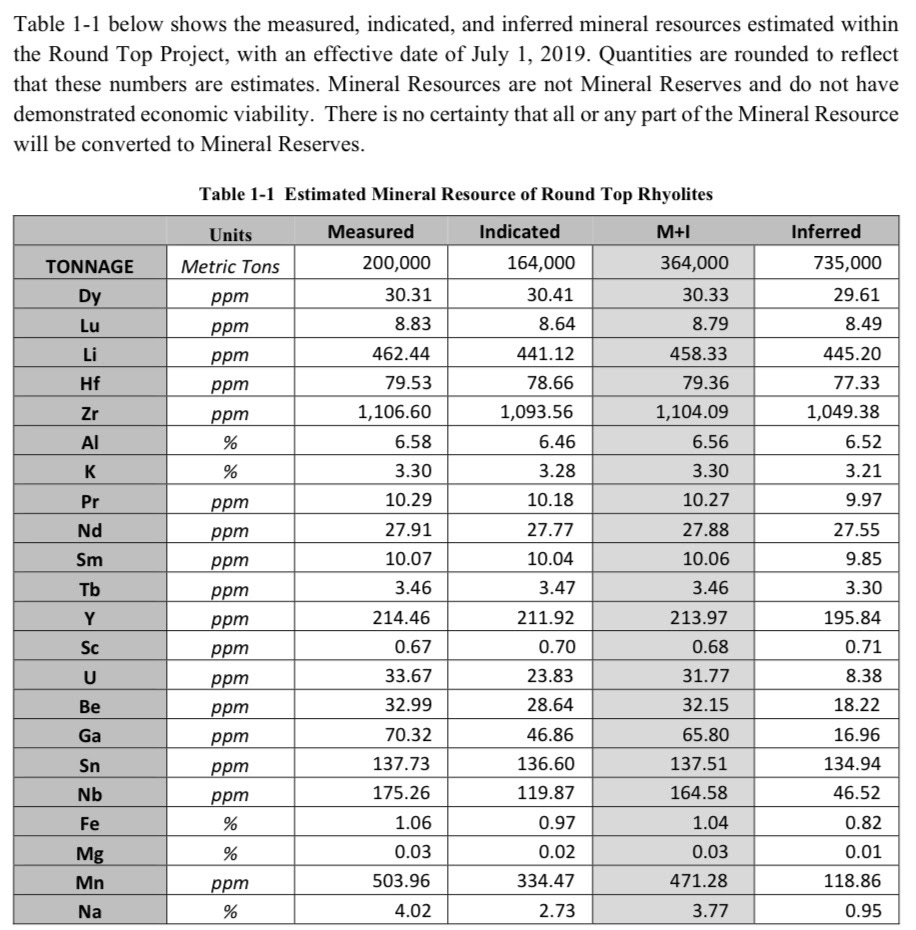

The research study gives us the estimated resources at the mine:

Again, I'm not a mining expert, but Rhyolite appears to be the base rock where the minerals are extracted from. Ppm means parts per million, a ppm of 1 means for every 1mm lbs of there is 1 lb of mineral.

Making some assumptions here, if we look at the total inferred resources for Round Top, it totals 735k metric tons. MP pulled 38,500 mt out of Mountain Pass in 2020, 38,500 X 20 years is 770k, which is a little more than the inferred resources at Round Top. Not all of these minerals are rare earths (like Lithium, still valuable), but the point is that Round Top resource capacity is at least similar to Mountain Pass.

The 2020 MP production number was actually 39% higher than 2019, and it is a much older mine, so assuming 2020 extraction level for 20 years would be impressive.

Approach #3:

Comparative analysis with MP Minerals. MP Minerals is the only other US based REM miner, so we can look at their market cap and try to make a comparison. This isn’t exactly one to one, mineral composition, margin, extraction and capex costs vary, but this is the best option from a comps perspective.

MP had revenue from REM sales of $134mm in 2020. When 2020 annual financials were released, the market cap was ~$7bn. That gave MP a revenue multiple of 52. Applying the same multiple to $79.2mm (20% of estimated Round Top revenue) gives an estimated market value of ~$4.1bn, a ~27x increase on current prices.

MP has ttm revenue of $275.02mm, a market cap of $6.71bn which represents a revenue multiple of 24.4x which would result in a $1.9bn for TMRC (396*.2*24.4), ~12x upside on current prices.

We can also use an operating profit multiple to gauge valuation range. I’m using operating profit since it requires less assumptions than ebitda for TMRC. Over the past 12 months, MP has had an operating profit multiple ranging from 40-100. If TMRC achieves target operating profit, these multiples would put the value at ~$2-5bn. It would take a 6,000 bp reduction in operating margin for TMRC and a multiple of 20 to essentially break-even on the investment.

NAV assumptions and a revenue/operating profit multiple aren't the best proxies for valuation. REM’s are not like other commodities. The market is small, with only one other domestic player and only recently considered a national security concern. The point here is to illustrate that if/once the Round Top mine and TMRC are treated as a cash flow generating business, the valuation has significant upside.

The big picture is that once the Round Top mine is approved, it will be worth significantly more than it is now. There are a multitude of ways the market could choose to value the resource, but it almost certainly will be a multiple of the current price.

It's Important to note that TMRC will need to take on some additional financing to get the mine operational. They will need ~$120mm (20% of initial capex and subsequent capex). MP Materials has an annual capex of $149mm, which is significantly higher than the $250mm (total over 20 years) projected for Round Top over 20 years.

Financing could be a combination of equity, convertible debt, debt, or partner financing with USARE. USARE has provided interest-free cash advances to TMRC of ~$550k in 2020 and 2021. Government subsidies are another option. In 2021, the US House of Representatives passed a $52bn subsidy package for domestic semiconductor production. A bill of similar function for REM is a distinct possibility.

Risk Factors

There are a variety of risks with this investment. I’ll list them out in order of likelihood and describe the downsides and mitigating factors.

Significant innovation in E&P (exploration and production) would be harmful to valuation. The core of the investment case is the scarcity of REM. If suddenly a massive REM deposit is discovered (think Permian basin in O&G industry),that would put downward pressure on the prices, diminishing the mine value. Additionally, new extraction technology that significantly lowers the environmental impact and cost of REM mining would have a negative impact. This would help TMRC’s margins as well, but increase total supply and competition if other deposits became more feasible as a result. There are a few other potential REM deposits in the US, but none with the depth of materials of Mountain Pass and Round Top.

The low market cap and trading volume may pose a risk to anyone attempting to build a position of size. A market cap of ~$150mm makes it challenging for an institution to build up a large position without moving the price. The position would have to be built up over time.

The Round Top mine may never become developed. This is the largest risk in terms of absolute downside, but the probability is low. If the mine doesn’t get approval, the stock is essentially worthless. I’d be surprised if this happened. TMRC and USARE are following the regulatory guidelines and the government has recently deemed REM essential. The government has collaborated with TMRC on preliminary research, and the Round Top mine is the only near development project in the USA, with a multi-year development period.

REM could become obsolete. If the minerals are no longer necessary then the value of the mine is 0. It is unlikely that a transformative manufacturing innovation with no prior R&D gets developed in the next 20 years.

Volatility in the spot pricing is another risk. TMRC is a miner and cannot control the price of their product. Unless more mines come online and demand tapers, it seems unlikely the spot price will have much downside volatility. Forbes cites REM demand for EVs alone being 10x the supply. Combine this with the geopolitical concerns and potential export curbs by China, and you have a shrinking supply and growing demand situation, which will have a positive impact on prices.

Conclusion

TMRC provides optionality in control of one of the most scarce and important raw materials of the 21st century. TMRC is one of two publicly available ways to invest in the US REM industry. MP Materials is the other publicly available investment, but is already a production mine, and has been operational for 70 years. With MP, the upside is limited to future spot pricing increases. MP also has Chinese ownership which could be a downside risk capital controls are imposed by the US government on sensitive assets. The value of TMRC’s 20% share of an operational mine at Round Top is not reflected in the current market cap, even when discounted for potential risk factors.

TMRC shares spiked to $8 (4x upside on current prices) in 2011 when they first received the lease for Round Top. Over the next year and a half, the price reverted down as the market processed the delays and environmental concerns. This is worth noting as it provides a some level of a benchmark valuation for when shareholders are optimistic about mine approval. Additionally, 2011 predates the currently understood significance of REM.

The energy transition, advanced technology, and national security protectionism are some of the most important themes of the 2020’s. REM’s are critical components of all three, and US government agencies have identified Round Top specifically as a vital resource. Historically, when resources are deemed important for national security, conditions for domestic producers become favorable.

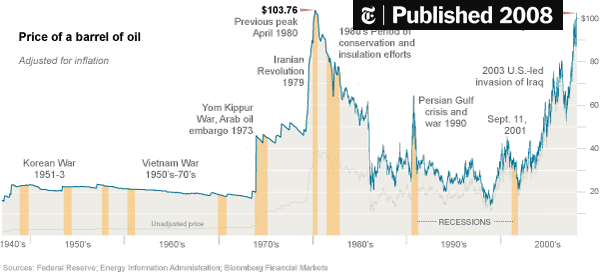

From 1973-80 oil exports from the Middle East were curbed because of geopolitical reasons & inflationary pressures. This put significant upward pressure on the price until the embargo was lifted in 1980.

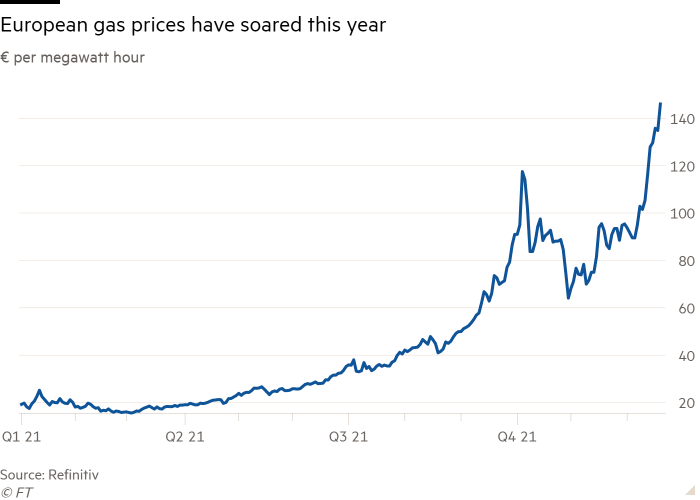

The recent natural gas price increases in Europe are also a potential template for the future REM situation. A combination of stronger than expected demand (cold winter) and geopolitics artificially limiting supply (Russia limiting gas exports) has inflated the spot price 7x (top). Cheniere Energy (bottom) is a US based producer of LNG. Cheniere was not hindered by export limits and saw share appreciation of ~68% in 2021.

A situation where China restricts REM exports to the US or the US restricts Chinese imports would have a similar effect on spot pricing. US REM miners would benefit.

In conclusion, the primary catalyst for TMRC is full mine approval. The mine is currently scheduled to begin production by 2023. Official approval from the Texas General Land Office would be the first major valuation expansion. Holding the investment past that could yield the benefits of spot price increases, or geopolitical supply constraints. There is the added possibility of TMRC’s 50.5% Santa Fe silver exploration project, the mineral reclamation facility becoming something or more grant income. Regardless, buying TMRC now and waiting for the approval likely has the most asymmetric upside.

Alex, are you still following TMRC/USARE? Just curious, with the updates over the past 12 months, I believe this is coming together. Although mining may not actually commence until next year or even 2025. With USARE series D funding wrapping up this month or so, I would anticipate some announcement of an IPO/ possible purchase/merger of TMRC and USARE. What are your thoughts on this at this time?